The Economic Legacy of Edward Heath: an Economic Crisis and State of Emergency

1970s union militancy, unemployment and inflation, aggravated by a Keynesian reflation, price and wage control, a profits crisis, combined to provoke a crisis of capitalism and political authority

‘The real situation today is that no incoming Prime Minister, if Mr Heath takes over, has in living memory taken over a stronger economic situation than we are handing over to him’

Right Honourable Harold Wilson June 1970

A superficially good economic inheritance

Edward Heath and his Conservative Party unexpectedly won the June 1970 British General Election. The headline in the Daily Express, playing up Mr Heath's hobby pursuit of ocean yacht sailing and racing, was ‘Skipper Ted comes sailing in’. Superficially the economy appeared benign. There was a surplus on the balance of payments, the Public Sector Borrowing Requirement had been eliminated and the exchange rate appeared competitive after a devaluation that was eventually accompanied by a domestic deflation to secure competitiveness.

Deep Structural Problems and growing problems in macro-economic management

Yet there were a series of structural problems in labour and product markets that would aggravate any macro-economic challenges that an incoming government might encounter. There were, moreover, plenty of awkward macro-economic problems ready to present themselves to the new Conservative Government. Part of the explanation for Edward Heath’s election success was rising price inflation that the public laid at the door of Harold Wilson’s Labour Government. In the election campaign Heath had effectively tapped into this distemper, memorably promising that a Conservative government would ‘cut prices at a stroke.’ While the comment on the abolition of Selective Employment Tax - ‘This would, at a stroke, reduce the rise in prices’ - was more nuanced, it played effectively to public concern about inflation.

As well as rising inflation it was becoming increasingly difficult for governments to meet the full employment commitment of the 1944 Employment White Paper. And certainly difficult to do so in the terms that post-war governments had come to accept as full employment, namely unemployment below 2 per cent. In the early 1970s as unemployment continued to rise the question that was increasingly debated was whether the government could stop unemployment from reaching one million on the claimant count.

The big problem in the 1970s: inflation

On 7 July 1970 the newly appointed Chancellor of the Exchequer Iain Macleod spelt out to the House of Commons Britain’s awkward inflation problem:

‘There is no doubt that by far the most serious problem that we face, not just as a Government but as a country, is inflation ….at present, contrary to past experience, we have the highest rate of wage increase for 20 years, although output is stagnating and unemployment remains high.

…..prices have also risen much more rapidly in the last two and a half years. A long-term look at this is, I think, instructive. Between 1958 and 1964 we had an annual rate of increase in this country in consumer prices of 2.2 per cent. Between 1964 and 1967 that rose to 3.7 per cent. I will come back to those figures. Then in each of the years 1968 and 1969 they rose by 5 per cent. In the three months to May 1970, the retail price index was 5½ per cent. higher than a year earlier.

Iain Macleod the Chancellor who died before he could deliver a budget

This was the only speech that Macleod delivered as Chancellor in the House of Commons. He never delivered a budget statement, dying suddenly in July 1979, holding office for hardly a month. It is not clear what Macleod would have done about inflation. The Conservative Manifesto, the so-called Selsdon Park Manifesto, was free market in orientation, rejecting the bailing out of lame duck industries and statutory prices and incomes policies. On inflation as Chancellor Macleod spoke of the dangers of high pay settlements, yet there was no hint of the sort of macro-economic and monetary conditions that could be constructed to stabilise the price level.

Macleod is now a distant figure; he is best remembered for his role as a liberal Colonial Secretary dismantling the British Empire in Africa and his political attack on the Magic Circle of Etonian Conservative politicians that arranged for Alec Douglas-Home to succeed Harold Macmillan as prime minister in October 1963. Yet he is an interesting figure. Gerald Warner in Iain Macleod — short-serving chancellor and lost Tory leader in October 2020 wrote an interesting and evocative blog about him. Macleod was a very articulate - fluent in speech and on paper - clever and acute man. Having read history at Cambridge he had trained as a lawyer. The most remarkable thing about him was his famed skill as a bridge player. After he graduated from Cambridge in the 1930s his annual winnings at the bridge table were in today’s money £140,000. Macleod, however, was not an economist and had little City or wider financial expertise. As far as I know he left no substantial comments on macro-economic or monetary policy such as on the Thorneycroft rows over public expenditure in 1958, the report of the Radcliffe Committee on monetary policy, the Maudling Dash for Growth in 1964, or the role of Domestic Credit Expansion controls as part of the IMF’s conditionality on lending to Britain in the late 1970s. Most of his effort as Shadow Chancellor had gone into planning tax reforms directed at lowering Britain's very high marginal tax rates and making corporation tax more coherent. These are a favourite occupation for Conservative politicians when they consider Treasury policy. Most of this thinking was implemented in the new government’s first finance bill in 1971.So it is not at all clear how Macleod would have dealt with Britain's inflation problem in the 1970s.

After Macleod’s death in July 1970 Edward Heath appointed Anthony Barber as Chancellor. Barber had obtained both a first class degree in law as an external student of London University, while he was a prisoner of war in Germany and a degree in Philosophy, Politics and Economics from Oriel College Oxford. Barber had benefited from the special ex-serviceman scheme of a shortened two year degree. My own economics tutor, Maurice Scott, had gone up to Oxford after the war on the same scheme. Barber went on to practice law as a barrister specialising in tax. He had served in previous Conservative governments as a Treasury minister and was well equipped to be a competent minister in an economic department. Barber was however both intellectually and politically a pedestrian figure. He is remembered as a Chancellor who was very much the economic assistant to the Prime Minister Edward Heath.

A Prime Minister by instinct committed to expansion advised by a civil servant in favouring a second dash for economic growth, much as Reginald Maudling in 1963-4

Edward Heath’s instincts were pretty much out of the Harold Macmillan play book, keep unemployment low, gow for growth, expand and have ambition. Of course the book in question is Harold Macmillan’s Middle Way. Heath’s thinking was stimulated or perhaps more accurately described as confirmed by Sir William Armstrong. Macleod in July 1970 had in effect described an economy where the wheels were coming off the post-war Keynesian macroeconomic consensus, but offered no resolution to its central problems of rising inflation and unemployment. In this context the Prime Minister and Sir William Armstrong were oblivious to the hurricane of inflation that could easily damage the British economy. While the Chancellor, Anthony Barber, was an intellectual bystander, best thought of as a technocrat managing the prime minister’s agenda.

Unemployment goes over a million

The first thing that went wrong and posed a problem for the Conservative government was unemployment hitting one million people on the claimant count. This resulted from the deflationary impulse that continued to run through the economy arising from measures taken by Roy Jenkins after sterling’s devaluation and the IMF conditionality. Throughout 1971 unemployment climbed to over a million. In January 1972 the the Department of Employment reported that the number of people claiming unemployment benefit had hit 1,023,583.

1972 A full scale Keynesian reflation - a second dash for growth by a Conservative Government

The response of the Heath Government was decisive and immediate. There was a full Keynesian fiscal reflation and an audacious plan to grow the economy out of inflation by increasing production and benefiting from economies of scale. Reginald Maudling, the Home Secretary, who had been Chancellor between 1962 and 1964, provided the Cabinet with two economic memoranda advocating an expansion in the face of trouble. In his memoirs Edward Heath explained how well argued and helpful Maudling’s advice was for colleagues.

The Chancellor, Anthony Barber, announced on 23 November 1971 a series of measures to reduce unemployment. They included bringing forward capital expenditure in the nationalised industries and in central government departments. In the Spring Budget in march 1972 taxes were cut by £1.2 billion, the borrowing requirement was allowed to rise to £3.4 billion and the budget measures were expected to add 10 per cent to economic growth over two years. The Chancellor Anthony Barber said the budget measures are ‘intended to ensure growth of output at an annual rate of 5 per cent between the second half of last year and the first half of next’. The Chancellor was not worried about the budget’s effects on inflation saying “I do not believe that stimulus to demand of the order I propose will be inimical to the fight against inflation. On the contrary, the business community has repeatedly said that the increase in productivity and profitability resulting from a faster growth in output is one of the most effective means of restraining prices increase’.

Fiscal Reflation 1971-74: Sevenfold Increase in Borrowing and a Doubling of Public Expenditure

Source BRITISH ECONOMIC POLICY 1979-74 Two View A View From the Outside, Ralph Harris IEA Hobart Paperback February 1975

A 5 per cent annual growth target that eclipsed the National Plan ambitions of 1963 and 1965

In March 1973 Barber introduced a ‘broadly neutral budget’ and he believed on this ‘basis the economy will continue to grow at an annual rate of around 5 per cent over the next eighteen months from the second half of 1972 to the first half of 1974’. The Public Sector Borrowing Requirement was forecast to be £4,423 million. This policy of going for growth through full scale Keynesian domestic demand stimulus received general support from the unions and from business and the CBI. The Times, then edited by Willaim Rees-Mogg said if anything that the government should be more expansionary, The Economist enthusiastically argued that the government had a determined leader, prepared to fight inflation and was about to make an economic breakthrough in terms of growth, and the National Institute Economic Review offered the government every encouragement in its policy.

A floating and devaluing exchange support expansion

By 1972 the Bretton Woods fixed parity regime had for all practical purposes collapsed. This made it relatively easy for the government to float sterling and break the $2.80 fixed parity against the dollar in June1972. Sterling was under pressure as a result of UK inflation, controversy over industrial relations being played out in the National Industrial Relations Court and the Court of Appeal, and a suitably unhelpful observation from the Labour Shadow Chancellor Denis Healey to the house of Commons Finance Bill Committee that devaluation was inevitable before the summer was out. This devaluation facilitated the ‘second’ dash for growth.This relieved the expansion from the immediate Achilles heel of the balance of payments constraint and a fixed exchange rate target. In effect it was the UK’s third post-war devaluation. Over the next four years to 1976 sterling would drop by 25 per cent against the dollar. The Index of Industrial Production that had hardly moved since 1969 rose 3 per cent in the second half of 1972 and by 7.5 per cent in 1973.

The 1972 Industry Act - the Spadework for Socialism?

The expansionary budget was accompanied by a new and revived industrial strategy. This was supported by the newly created National Development Executive based in the Department of Trade and Industry that was planned to spend millions of pounds on new industrial initiatives. The approach that had been laid out in the White Paper” Industry and Regional Development” was translated into the Industry Act 1972. This reflected Edward Heath’s view that British industry had to be prepared for the European Common Market that the UK would be joining on 1 January 1973. The core thinking behind the Industry Act had been laid out by Sir William Armstrong at a meeting in Chequers November 1971. His view according to Sir Donald MacDougall, the Head of the Government Economic Service and Chief Economic adviser, who was there was that ‘we should think big, and try to build up our industry onto a Japanese scale..This would mean more public spending. We should ask companies what they need in the way of financial and other help, and give it to them.’

The Industry Act 1972 gave the government much broader power of industrial intervention than anything conceived by the Wilson Labour Government’s controversial Enterprise Act 1968. It was conceived, in the view of Sir Leo Pliatzky, as a measure to ‘strengthen our industrial capacity so as to take advantage of membership of the Common Market.’ Sir Henry Legge Bourke the Chairman of the 1922 Committee - the name given to the Conservative Parliamentary Party that excludes ministers - described it as a socialist bill by ethic and philosophy and obnoxious. While Mr Tony Benn - the former Anthony Wedgwood-Benn - the left-wing Labour MP and former Minister for Technology in the Sunday Times under the provocative headline Heath's spadework for socialism wrote that this was ‘the most comprehensive armoury of government control that has ever been assembled for use over private industry, far exceeding all the powers thought necessary by the last Labour government...Heath has performed a very important historical role in preparing for the fundamental and irreversible transfer in the balance of power and wealth which has to take place’.The new powers were used to assist a huge range of companies. They included ICL computers, traditional industries such as Mersey Docks and Harbour Company, Govan Shipbuilders and Cammell Laird.

The Ted Heath U-Turn on the Selsdon Free Market Manifesto

The focus of this article is on the economics of Edward Heath’s Conservative government between 1970 and 1974. Yet the political context of its Selsdon Park Manifesto that the Conservatives fought the 1970 election on and its disjuncture with the conduct of the Government in office was egregious. The Conservative Party ran on a radical free market manifesto drafted after a meeting at the Selsdon Park Hotel in Croydon. It had several specific dimensions. These included radical reform of trade union law that went beyond the proposals of the In Place of Strike White Paper published by Mrs Barbara Castle in 1969, but abandoned by the Labour Cabinet, the abolition of statutory controls on prices and incomes and an end to government support for failing or lame duck companies. The political story of the Heath Government was that of the U-turn on prices and incomes policy and on the rescue of lame duck companies such as Upper Clyde Shipbuilders.

In many respects the U-turn on prices and incomes policy was the most significant decision economically because controls on prices, dividends and wages affect the whole of the economy. It brought the government into every board of directors and every work place deciding prices of products and wages and salaries. It was an attempt to repress increasing inflation. To work it required the co-operation and active support of the trade unions and their members. The circumstances for an effective pay policy could not have been worse. The Trade Union Congress and union leaders in general were bitterly opposed to the Industrial Relation Act passed in 1971 and openly defied judgements from its new National Industrial Relations Court. Even if the leadership of the unions had been prepared to help the Conservative Government their workers were not. Part of the reason for setting up the Donovan Royal Commission on trade unions was concern about the behaviour of workplace committees of shop stewards and the growth of wild cat and unofficial strike action that was not organised or sanctioned by unions. Edward Heath’s internal Conservative Party opponent and bete noir, Enoch Powell provided a devastating critique of the government. Powell asked ‘does the Prime Minister not know that it is fatal for any Government or Party to seek to govern in direct opposition to the principles on which they were entrusted to govern? In introducing a compulsory control of wages and prices, in contravention of the deepest commitments of this Party, has the Prime Minister taken leave of his senses?’

Industrial Relations Act 1971

In many respects the 1971 Act gave effect to the previous Labour Government’s White Paper “In Place of Strife”. The Industrial Relations Act went further than the White Paper. It brought in legally binding collective agreements, legally enforceable procedures for negotiation, compulsory cooling off periods and the creation of a new specialist court [the National Industrial Relations Court] to adjudicate on the operation of the new legislation. There was a greater opportunity to make collective agreements with 'no strike' clauses. Trade unions had to be registered to enjoy legal rights and to enjoy legal immunities. Continued registration, moreover, required an organisation to meet specified criteria such as having rules that specified how, when and by whom, authority was exercised, particularly when strike and other industrial action was being taken.

Conservative ministers did not perceive the Act as an anti-trade union measure directed at reducing effective trade union power. Instead they thought of it as a positive piece of employment legislation that would lead to a better balance of industrial relations in a workable modern legal framework. This would empower trade unions to work with employers and government in a positive and productive manner appropriate for an advanced industrial economy. This thinking had informed Sir Andrew Shonfield in his note that formed part of the Donovan Report. It also had shaped Mrs Castle’s thinking when she had been Secretary of State for Employment and Productivity drafting the Labour Government’s response to the Donovan Commission. Both Mrs Castle and Mr Wilson were from the old Bevanite wing of the Labour Party that had been opposed by right wing trade union leaders. In Mrs Castle’s view they were often socially irresponsible in terms of wider social and economic considerations and needed to be pushed into a position where they could make a positive contribution to managing society, working with employers and government. In his memoirs Edward Heath explicitly comments that reducing trade union power was not the purpose of the Industrial Relations Act.

If the TUC and trade unions were not minded to co-operate with a Labour Government in changing industrial relations law and bring their actions within the management of the courts, they were not minded to accommodate a Conservative Government on the same mission. In Place of Strife had been bitterly opposed by the unions and the left in 1969. They had defeated it and been empowered by that defeat. In response to sharply increasing prices, the main purpose of unions was to protect the real wages of their members.

The Industrial Relations Act took effect in January 1972. It was put to the test on two occasions. In April 1972 in response to a proposed railway work to rule, the Secretary of State for Employment - Maurice Macmillan, Harold Macmillan’s son - applied to the NIRC for a cooling off order. The Government succeeded in obtaining a fourteen day cooling off period. At the end of that period the Government applied for a further order from the court and a compulsory ballot of the union members on the offer on the table from the employer. The ballot was held and the result was a vote of three votes to one for continued industrial action. Sir Geoffrey Howe QC the Solicitor General, who had taken the legislation through parliament and argued case before the NIRC, offers a concise account of the operation of the Act in his memoirs “Conflict of Loyalty”. The two remedies Sir Geoffrey had applied for drew on Mrs Castle's proposals in 1969 borrowing on American experience with similar remedies. His view is that ‘our mistake had been not in our design but in our use of them. We were wrong to believe that we had to use both in quick fast accession in the same dispute’.

The ‘second mishap’, as Sir Geoffrey put it, arose out of a longstanding dispute between dockers and road hauliers over containerisation. As well as ending up a cause celebre in the unworkability of the Industrial Relations Act in the early 1970s, the dispute illustrated the industrial relations obstacles to technological innovation and economic modernisation. In constructing the Industrial Relations Act the Conservative Government worked hard to ensure that only trade union organisations would be caught by the terms of the Act. No individual person would be brought to the court and held personally responsible for an action or indeed exposed to imprisonment for contempt of court. The gravemen of the litigation was that dockers were ‘blacking’ container trucks. Sir John Donaldson as President of the NIRC held this to be an ‘unfair industrial practice’. The Transport and General Workers Union TGWU were ordered to pay a fine of £55,00 by the NIRC, acting as the court of first instance. The TGWU took the case to appeal and the Court of Appeal with the lead judgement being given by the Master of the Rolls, Lord Denning MR - in effect the chief justice of the civil division of the English High Court - quashed the NIRC order on the grounds that the TGWU union had not organised the action and were not responsible for it, implying that the remedy should be sought against the individuals making the action. Within six weeks the Court of Appeal decision was reversed by the Judicial Committee of the House of Lords - at that time the supreme appellate tribunal in the UK - restoring the law to that envisaged when the law officer piloted the legislation through Parliament. Between the Court of Appeal decision and the House of Lords decision the NIRC applied the law as declared by Lord Denning MR. This resulted in penalties being applied to individual trade unionists by the NIRC. This resulted in three London dockers being sent to prison. This was easily portrayed as martyrdom writ large, and there was extensive sympathy strike action and political demonstrations. The men were released from prison as result of an application by the Official Solicitor, until then a publicly unknown government functionary who applied to the Court of Appeal for the dockers release. The application was suggested by Lord Denning MR to the Counsel for the men belonging to the TGWU, Peter Pain QC. The Court of Appeal led by Lord Denning MR quashed the NIRC judgement, on the grounds that the evidence before the NIRC had been insufficient for its decision.

Sir Geffrey Howe’s concluding comments on the episode are an example of judicious understatement that reflected his character and temperament. Sir Geffrey wrote in his memoirs that ‘‘Parliament, at our bidding, had intended liability for unfair industrial action to fall not upon the individual trade unionists but upon the funds of these giant organisations, which had since 1906 been immune from liability. That was the central mischief at which the Act was directed. And the Court of Appeal, by setting that aside, for six fatal weeks until the Lord's restored the position, had torpedoed the fragile vessel, which Robert Carr, Stephen Abbott and I had so carefully designed’. After this for all practical purposes the Act was dead.

Any large scale and rapid inflation would usually be a recipe for workplace trouble. In the early 1970s this inevitable trouble was aggravated by two further things. The first was the consequences of the various efforts to run pay policies in the 1960s. These had compressed pay differentials and set off all sorts of anomalies that unions would want to rectify. The second was a changed radical political climate that was novel in British industrial relations. This partly reflected the political radicalism present in western Europe and North America. It was political and it was militant. This trade union militancy was evocatively expressed in the pop song Part of the Union produced by the band the Strawbs and released in 1972, making it to Number 2 in the charts in 1973 with the band appearing on Top of the Pops in February 1973. The lyrics are worth reading

Now I'm a union man

Amazed at what I am

I say what I think, that the company stinks

Yes I'm a union man

When we meet in the local hall

I'll be voting with them all

With a hell of a shout, it's "Out brothers, out!"

And the rise of the factory's fall

Oh, you don't get me, I'm part of the union

You don't get me, I'm part of the union

You don't get me, I'm part of the union

Until the day I die, until the day I die

As a union man I'm wise

To the lies of the company spies

And I don't get fooled by the factory rules

'Cause I always read between the lines

And I always get my way

If I strike for higher pay

When I show my card to the Scotland Yard

And this is what I say

Oh, oh, you don't get me, I'm part of the union

You don't get me, I'm part of the union

You don't get me, I'm part of the union

Until the day I die, until the day I die

Before the union did appear

My life was half as clear

Now I've got the power to the working hour

And every other day of the year

So though I'm a working man

I can ruin the government's plan

And though I'm not hard, the sight of my card

Makes me some kind of superman

Oh, oh, oh, you don't get me, I'm part of the union

You don't get me, I'm part of the union

You don't get me, I'm part of the union

Until the day I die, until the day I die

You don't get me, I'm part of the union

You don't get me, I'm part of the union

You don't get me, I'm part of the union

Until the day I die, until the day I die

Prices and Incomes Policy, greater market competitive product and labour markets and inflation

The Government abolished the National Board for Prices and Income ( NBPI) in November 1970 ending Labour’s prices and incomes policy. The Government’s first economic priority as the Chancellor Anthony Barber explained to the House of Commons in the March Budget in 1971 was ‘to defeat inflation’. There were suggestions that inflation could be controlled by more competition in the economy and through the reforms of the Industrial Relations Act. There was a pay policy for the public sector if not for the economy as a whole. New review bodies were planned to make recommendations for different parts of the public sector.The public sector pay policy was based on the N-1 formula where each pay settlement was to be at a rate lower than the previous. In his 1971 Budget speech the Chancellor expressed concern about inflation and unemployment. Describing both simultaneous higher inflation and higher unemployment as ‘baffling’ and ‘paradoxical’. While acknowledging the dangers of lax monetary conditions Anthony Barber found no reason ‘ to restrict the growth of the money supply so as to reduce demand below the level needed to achieve a growth of output in line with the growth of productive potential’. Inflation control was to turn on a combination of wishful thinking about an improvement in the economy’s micro-economic efficiency, exhortation about wages and eventually a return to formal incomes policy.

In Planning and Politics: the British experience 1960-76 Sir Michael Shanks suggested that much thinking in Britain in the early 1970s on pay policy was coloured by the perceived successful course of President Nixon’s administration in the United States. President Nixon had taken office on a platform of laissez faire. Yet unwilling to tolerate high levels of unemployment and wanting to reduce inflation, President Nixon made a spectacular U-turn in 1970. The Nixon administration brought in expansionist policies, buttressed by measures to restrain wage increases and limit profit margins. In 1972 these measures appeared to have some success and had, in Shanks’s view, considerable influence with the Conservative government. In the autumn of 1972, the work to prepare for prices and income policy was led by the National Economic Development Council and its new director general Sir Frank Figgures, a former ‘Treasury knight’, who would become chairman of the pay board.

Sir Michael commented that ‘in September the working parties reported to an NEDC steering group, consisting in effect of the Council less it's independent members, chaired by the Prime Minister at Number 10 Downing Street. Mr Heath's handling of the operation was masterly. Not only did he begin to convince a suspicious TUC of the genuineness of his desire for a consensus but as the negotiations went on he seemed also to convince himself that the country could be run on the basis of mutual trust and cooperation between a Conservative government and a strong but responsible trade union movement’. In order to court TUC support for a pay policy the Government accepted that its capacity to order macroeconomic policy priorities would be constrained. The Prime Minister pledged to maintain a programme of high growth despite the problems of inflation, a plummeting exchange rate and a deteriorating balance of payments.

The introduction of a statutory prices and income policy in the Autumn of 1972 put the Government on a collision course with the unions. In the Mixed Economy of the post-war years any government was likely to meet trade union opposition in its role as a public sector employer. The government not only framed the employers side wage negotiations for the civil service, local authorities, police and armed services but also for the nationalised Industries. This meant all the major utilities, railways, steel, telephones and coal were potential sources of direct conflict over pay.

When the Conservative Government first came to power it abolished Labour’s statutory Prices and Incomes policy. This was a manifesto commitment carried out in 1970. The Government, however, sought pay restraint in the public sector. Ministers also welcomed the employers’ organisation, the CBI’s, voluntary private sector pay guidance of wage and salary increases of no more than 5 per cent. By the summer of 1972 it was clear to Conservative ministers that, given the inflation problems, if their chosen policy instrument - pay restraint were to work it would have to be imposed by law. The TUC was not minded to co-operate with the Government but, even if trade unions had been minded to work with the government on pay restraint, it would have been harder to sell a pay policy to their members as ‘imposed by law ‘ rather than a policy that they had embraced.

There were two Counter-Inflation Acts. The first, the Counter-Inflation (temporary provisions ) Act 1972 imposed a 90 day freeze on pay, prices, rents and dividends. This was the first phase of the pay policy, The second phase, the Counter Inflation Act 1973, involved a much more elaborate and ambitious management of pay pressures. Pay was in principle to be increased by no more than £1 plus 4 per cent and pay agreements could not be reopened within a year. The Counter Inflation Act 1973 established a Prices Commission and a Pay Board. These had powers to invoke criminal sanctions with the permission of the Attorney-General. The scope and detail of the legislation is suggested by the commentary on the act in the Oxford Industrial Relations Law article published in June 1973 Counter-Inflation Act 1973 ‘During stage two prices and pay are governed by the principal set out in the price and pay code, itself you have another example of the increasing trend towards the use of rules which are not laws in the sense of rules that breach of which involves the commission of a legal role but which are not entirely without legal consequences. First it is indisputable that several of the terms used in the code are shrouded behind an impenetrable penumbra. What is “a group of workers“? Who are the low paid? When is the principle of capability acceptable? The chairman of the Pay Board, Sir Frank Figgures, has acknowledged the vagueness of some of the terms of the code on principal increases. He noted that the code is not especially helpful. It does not define the word principal and neither do we. Secondly, the price commission and the pay board had discretion to modify or alter the provisions of the code to meet particular circumstances’. The legislation was a recipe for complexity, muddle, ambiguity and contention. What could go wrong, would go wrong over the next two years. What ministers would say was certain and necessary during the course of disputes would deus ex machina become unnecessary and easily overridden.

Phase 3 announced in October 1973 and taking effect on 7 November 1973 was more complex because it embodied greater flexibility. To build support from the unions Edward Heath had again at a meeting with the NEDC pledged that “This time we are determined to sail through the whirlpool’ Edmund Dell observes in the Chancellors that ‘flexibility, though probably Inevitable after a year of strict unalterable rules under Phases 1 and 2, is the death of incomes policy. The revised pay norm was a 7 per cent increase or £2.25 for the lower paid workers and extra pay to sort out anomalies, rewarding merit, taking account of the higher cost of living in London, and the unpleasantness of ‘unsocial hours’. An important example of its additional flexibility was the incorporation of a cost of living adjustment - the principle of a ‘threshold’ agreement. If the Retail Prices Index rose by 7 per cent above its October level during the next 12 months workers were entitled to automatic wages increases in compensation, on the basis of a formula where wages rose 1.2 per cent for each 1 per cent rise in prices above the threshold. Sir Michael Shanks records that the Conservative Government thought that increase in productivity of 3-4 per cent would keep price increases below the threshold. As it turned out the threshold was reached in April 1974 and the threshold agreements went on to raise wages by £4.80 a week.

Edmund Dell, writing from the perspective of a former Labour Cabinet minister and historian, observed in his book The Chancellors that ’There was now a statutory prices and incomes policy. But as it derived from an attempt to mobilise the voluntary support of the unions, it could itself only be inflationary. All the costs of buying union support were paid without even such benefits as Union support might have provided.’

The collapse of Bretton Woods, expanded dollar liquidity, American led inflation a synchronised international economic business cycle and booming commodity prices

The full scale reflation of the British economy in 1972 started against a dramatic international background. The post-war Bretton Woods international payments system collapsed when Richard Nixon closed the gold window in 1971. Countries had scope to manage their exchange rates in a manner consistent with their domestic economic priorities. Britain took the decision to float sterling in July 1972. The collapse of the system came about because of the financial instability of the metropolitan currency at the heart of Bretton Woods: the dollar. `The combination of rising US prices and a weakened US balance of payments vitiated the practical capacity of the US Treasury Department to stabilise and manage the dollar based system. It enabled economies such as the West German Federal Republic, Japan and Switzerland to break with the dollar and avoid importing American inflation into their economies. US monetary and fiscal policy remained loose expanding international dollar liquidity. This contributed to a synchronised economic expansion in advanced economies, amplifying the UK’s domestic stimulus, for example, and contributed to a simultaneous boom in commodity markets. The price of some commodities doubled in price over a two year period.The UK’s terms of trade deteriorated sharply. The prices of its imports rose relative to its exports and sterling fell against the dollar and other currencies such as the deutschmark and the yen. This potent combination contributed to a pass through of higher international prices into the domestic UK prices. The distinctive structure of Phase 3 of the UK Prices and Incomes Policy with a significant degree of indexation through the threshold arrangements, inevitably ensured these higher costs were passed into the cost structure of UK prices.

The Arab-Israeli War and the Oil Price Shock 1973

These effects would entail extremely awkward external price shocks without any other factor in play.Yet in November 1973 as a result of political consequences of the Arab -Israeli Yom Kippur War, the OPEC oil producing cartel quadrupled the price of oil. . This was both an immediate price shock that would raise inflation and potentially an internationally deflationary shock that would transfer dollar liquidity to economies that were potentially unable to deploy their increased dollar income in either consumption or investment spending. The effect was to take around $50 billion from oil consuming economies.The immediate advice of the Treasury and the Government Economic Service was to continue to borrow to support the balance of payments and not to allow this international oil shock to derail the UK’s government’s determination to raise its rate of growth. The OPEC oil shock amplified the economic ‘whirlpools’ beyond anything the NEDC could have imagined when the Prime Minister made his comment and committed the government to the expansion that had been embarked upon in 1972.Sir Donald MacDougall, the Treasury’s chief economic adviser moved to work for the CBI in December 1973 and gave the employers organisation the same advice that had he given Treasury ministers. The oil price shock had an immediate effect on Stage 3 of the government’s pay policy. It meant that the pass through to the RPI from higher energy costs would within months create inflation that would trigger the ‘threshold’ provisions of the pay policy, automatically escalating domestic cost pressures. The Chancellor Anthony Barber made some limited deflationary measures in a mini-budget in Autumn of 1973. These included restrictions on hire purchase credit, an increase in surtax on the top rate of income tax and £1,200 million of expenditure cuts planned for 1974-75. Yet, given the scale of the shock these were modest. Edward Heath and his ministers were broadly content to follow the advice of Sir Donald MacDougall.

The Industrial Relations Act 1971 along with the government’s public sector pay policy with its N-1 formula and the statutory incomes policy announced in November 1972, inevitably brought the Government into conflict with the trade unions. Union leaders, businessmen, civil servants and ministers could talk as much as they liked at the NEDC, but what mattered to unions was the pay of their members. Pay packets , moreover, were being destroyed in terms of real purchasing power by high and accelerating inflation. The Chancellor Anthony Barber may have informed Parliament that inflation was his principal priority, but for a trade union negotiator getting an above inflation pay rise was a much more pressing concern. Their whole purpose and rationale was to protect their members' real pay and to obtain as large a share of national income for them as possible in an expanding economy.

Things started in 1970 pretty much as they were to go on. Public sector unions were not prepared to abide by the N-1 pay guidance. If they had sufficient industrial muscle they did not hesitate to use it to get what they wanted. In December the power workers at the nationalised Central Electricity Generating Board started a work-to-rule in pursuit of a 25 per cent pay claim. The industrial action was settled by a Court of Enquiry chaired by Lord Wilberforce, a member of the Judicial Committee of the House of Lords. The power workers settled for 15 per cent. The National Union of Mineworkers (NUM) voted for strike action to restore their real pay differential in relation to other workers. This was the first official miners strike for nearly fifty years. Their pay claim could not be met within the terms of the N-1 formula. Negotiations over the National Coal Boar’s offer of 7.9n per cent and the promise of a backdated deal for an increase in productivity broke down. The miners comprehensively defeated the Government in a six week strike that started in January 1972. Flying pickets blockaded power stations so that coal that had already been mined could not be used in electricity power generation. 1972 was not the first instance of flying pickets. The tactic had been deployed in an unofficial mining dispute in 1969, but as an effective method of intimidation it was perfected by Arthur Scargill and his colleagues from the South Yorkshire coalfield. The result was huge disruption. Seventeen schools dependent on coal fired heating were closed within days in Shropshire and factories laid off workers because of power shortages. In total over 1.2 million people were laid-off. Given that three quarters of electricity was then generated by coal fired power stations there were power cuts. The power cuts took place on a rotating basis. My housemaster at school did not rust us in the dark. So we were taken by coach from Totnes to another town in Devon Paignton where the electricity was still on. To occupy us we were taken to see “The Good the Bad and the Ugly”.

On 9 February 1972 the Prime Minister obtained a declaration of a state of emergency.The Government again sought the assistance from an inquiry led by Lord Wiberforce. He recommended a pay increase of 27 per cent. The NUM agreed to settle on Lord Wilberforce’s terms and extracted an additional 15 beneficial conditions from the National Coal Board above the inquiry’s recommendation. The result was a complete humiliation of the Conservative Government. The government and the nationalised industries involved were poorly prepared for the coal strike in terms of maintaining coal stocks and deploying the coal that was available. The police response was wholly inadequate, accommodating NUM pickets when they chose to stop the Central Electricity Generating Board from using coal that the board had already purchased for generation in their own power station. The UK Cabinet Office's present emergency planning and coordination arrangements emerged from the review into this episode.

The settlement agreed in February 1972 with the NUM was due to lapse at the end of 1973. Sir Michael Shanks wrote that the TUC had been given to understand that Phase 3 of the income policy would be constructed to accommodate an exceptional pay increase for the miners. In November the NUM rejected a pay offer from the NCB of 13 per cent which appeared to deploy all the flexibility Phase 3 allowed and was almost twice the 7 per cent pay norm in Phase 3.. The NUM were determined to test the Conservative Government’s resolve on their public sector pay claim. Empowered by the quadrupling of oil prices, the miners embarked on an overtime ban in pursuit of a pay claim of 35 per cent. This overtime ban halved coal production and resulted in coal stocks falling as mid-winter approached.The Government declared a state of emergency and instituted a three day week to try to avoid power cuts, Television broadcasting was stopped at 10.30 pm in the evening. The NUM held a ballot for a full stoppage of work and received authority for strike action at the end of January 1974. The vote to strike in the ballot was an overwhelming 80 per cent.

The crisis of British company profits in the mid-1970s

The combination of high and rising inflation, price controls and rising wages destroyed the profitability of British industry. The micro-economic measures taken to suppress inflation did as much damage as the social and economic damage of inflation itself. As well as the malign consequences for incentives in product and labour markets that arose from blunting incentives and the information that would normally be yielded by price signals, the controls operated to eviscerate company balance sheets. Companies were not able to pass on higher costs from pay, the lower exchange rate and increases in commodity prices such as metals that had doubled and oil that in 1973 quadrupled. Much of the British manufacturing industry had faced competitive pressures that contributed to Britain losing international market shares in exports.The toxic combination of price controls and higher costs significantly further weakened their balance sheets. British experience of controls such as pay and price controls to repress inflation illustrated the way in which controls to blunt inflation create as much economic damage as inflation itself

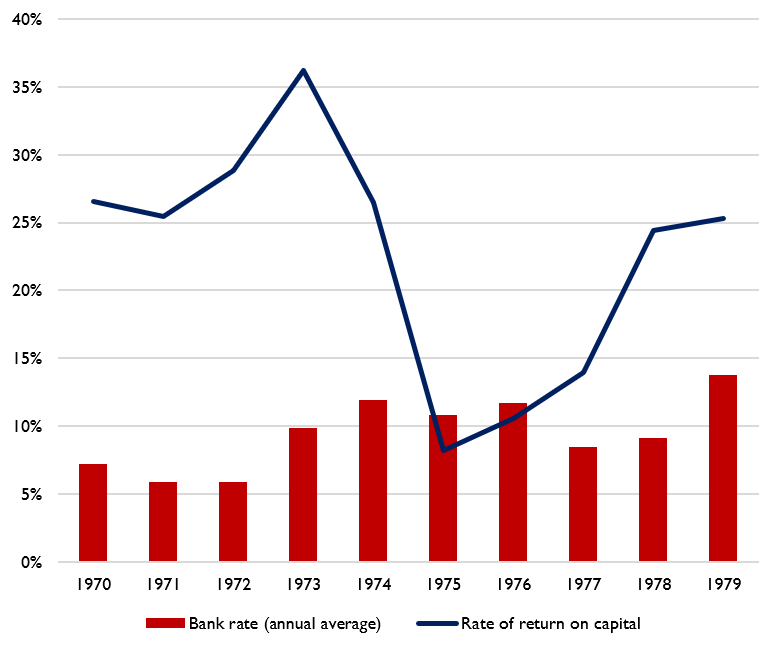

Profitability and interest rates 1970-79

(Profitability data from ONS dataset ‘Volume index capital services (VICS), annual, UK’, 9 November 2023; and interest rate data from Bank of England, ‘Research datasets: A millennium of macroeconomic data’, 2016)

Source House of Lords Research Note The Uk Economy in the 1970s April 2024

Marxist economists, such as Andrew Glynn were swift to recognise the structural vulnerability of British capital in the 1970s. While profits initially rose during the Barber Boom between 1972 and 1973s, unemployment fell as the bargaining power of labour rose. Inflation rose, commodity prices rose and the effect of the combination of price controls and rising pay aggravated by the threshold clauses of the Phase 3 of the Incomes Policy that acted as effective pay escalators, the effect on company balance sheets was devastating. This increased the labour share of national income to 67.8 per cent in the first quarter of 1974. By the third quarter of 1975 the ratio of labour income within the national accounts rose further to 71.9 per cent. The consequences of this is spelt out in a House of Lords Research Note published in April 2024 on the UK Economy in the 1970s, The rate of return on capital which had risen to over 35 per cent at the height of the boom in 1973, crashed to around 10 per cent in 1975. This was lower than the interest rate set by the Bank of England, reducing incentives for productive investment. As a share of GDP private investment fell by almost a quarter between 1973 and 1976 from 14.9 per cent to 11.4 per cent.

Price and income controls in the 1970s made an inflation problem worse

Milton Friedman understood his experience working in the US Treasury Department during the Second World War when comparable controls were used to manage wartime inflation. Friedman had also taken an interest in the work of one of his colleagues at Chicago University who had studied the effects of the Weimar hyperinflation in Germany in the 1920s. This work showed that the damage of this extraordinary episode of inflation was less than might have been expected. Apparently a key part of this was that the German Government did not resort to price or pay controls. This meant that price signals albeit blunted and less clear than normal because of the inflation continued to operate. They were not overridden by distorting and ineffectual regulation. Milton Friedman was therefore very critical of the Nixon administration for resorting to them in 1971. He was also very critical of his close friend Arthur Burns the Chairman of the Federal Reserve Board, who advised President Nixon to use price and pay controls

Pay Board cocks-up estimates of miners’ pay relativities and a ‘Farcical Election’

For several months the Pay Board chaired by Sir Frank Figgures had worked on a report on pay 'relativities'.The Pay Board on 19 February 1974 announced that their work on pay relativities had overestimated the pay of the miners, and that they were £3 worse off than the Pay Board’s statistical analysis had suggested.This arose because miners’ holiday money was scored as part of their remuneration whereas other industries excluded them.The overall result was that miners were earning about 8 per cent less. This suggested that the Miners’ pay claim could have been accommodated within the terms of Phase 3 of the Incomes Policy after all. This caused the Prime Minister Edward Heath acute embarrassment in the final stage of the “who governs Britain” election he called in February 1974. In his memoirs he provides a lucid account of the matters involved and their political consequences. The clarity of his writing on the matter also reflects Heath’s own experience in pay matters as a former Minister for Labour. Heath points out that there were ‘well established reasons for this apparent anomaly’. There were other items the miners benefitted from such as concessionary coal - that the Inland Revenue did not apply the normal benefit in kind rules of income tax to under a longstanding Extra Statutory Concession - that had not been taken into account in the Pay Board’s calculation.Heath with great irritation wrote It appeared to show, wrongly as iturend out, that the miners were worse off than even the NUM thought. The press had a field day, suggesting that the government had made a calculating bungle with regard to the main issue upon which the election was being fought.Harold Wilson claimed that an arithmetical error had thrust the country needlessly into a national pit strike, the resultant disruption and what he turned a farcical general election’. On 28 February Edward Heath’s Government was defeated in the general election and a minority Labour government led by Harold Wilson took office.

Competition credit control, monetary policy and inflation.

In this survey of the economic policies of the Heath Government there has hardly been a mention of monetary policy or monetary growth. The Prime Minister and his economic ministers such as Peter Walker and Ian Gilmour were fully committed to the post-war Keynesian macro-economic orthodoxy. A monetary analysis played no part in the economic policy against inflation which from the start the government had identified as its principal policy priority. In May 19971 the Bank of England published a consultative document on Competition Credit and Control. This removed quantitative limits on bank lending.The chief economic adviser at the Treasury Sir Donald MacDougall considered the scheme inherently inflationary. The proposal was part of a reform of the Bank Rate to supposedly make interest rates more market- oriented with the Minimum Lending Rate replacing the Bank Rate. The idea was that there should be greater use of open market operations to set interest rates. Treasury ministers were advised that if quantitative controls were to be removed greater use would have to be made of interest rates to control monetary conditions. Ministers apparently welcomed the change from direct controls because they favoured the use of the price mechanism.

MacDougall explains in his memoirs that when Ministers had to make decisions on interest rates in order to control monetary growth by choking off the demand for money by increasing rates, they were reluctant to act and moved too slowly and insufficiently. The failure to implement the necessary increases in interest rates contributed to an explosion in the money supply. Loose and accommodating monetary policy became part of the government's economic purpose. In his Budget speech in March 1971 the Chancellor Anthony Barber, for example. noted that ‘this Budget will entail a growth of money supply that is high by the standards of past years, in order to ensure the adequate finance is available for the extra output. To proceed otherwise would reduce the growth of real output itself.” The growth of M3 rose from 10.4 per cent a year in 1970-71 to 38.1 per cent in 1972-73.

UK Money Supply and Inflation 1967-74

Source BRITISH ECONOMIC POLICY 1979-74 Two View A View From the Outside, Ralph Harris IEA Hobart Paperback February 1975

No formal prices or incomes policy could have suppressed inflation in the context of the monetary explosion that took place between 1971 and 1974. Moreover the whole of macro-economic policy cohered on one objective: growth of 5 per cent in GDP a year. In British Economic Policy 1970-74 published in February 1975 Ralph Harris the Director General of the Institute of Economic Affairs (IEA) set out a devastating indictment of the conduct of monetary policy. Lord Harris concluded that the cause of the inflation rested with the government’s monetary policy writing that ‘even among those who put the primary blame on trade union ‘pushfulness’ it may be agreed the Conservative Government’s expansionist monetary policy immensely strengthened the effective power of trade unions and others to press for wage and salary increases without having to worry about the danger of unemployment which is now coming home to roost’ Between 1970-71 and 1974-75 public expenditure doubled from £22 billion to £42.8 billion, the Public Sector Borrowing Requirement rose sevenfold from £617 million to £4.2 billion.The decision to float sterling in the summer of 1972 further accommodated the combined monetary and fiscal expansion.

Money Supply and Inflation 1968 to 1974

Source BRITISH ECONOMIC POLICY 1979-74 Two View A View From the Outside, Ralph Harris IEA Hobart Paperback February 1975

The British economic establishment - the Treasury, the Bank of England, the Government Economic Service and the academic network of Oxbridge economists that advised it - continued to be fully invested in the intellectual legacy of Lord Keynes. One of their collective puzzles in the post-period of disappointing relative economic performance, was how a political and policy making community that benefited from the great intellectual heritage that Keyens bequeathed managed to do so badly compared to other comparable advanced industrial economies. The awkward problem that was becoming apparent in the early 1970s was that the answer to that plaintive question was located in Lord Keynes’s legacy and the neo-Keyensian application of it.

Some intellectual dissent began to emerge among British economic commentators. Professor Alan Walters in the Joseph Sebag Newsletter, for example, condemned the ‘explosive money supply’ writing that ‘the implications are perfectly clear and that inflation will continue at a somewhat increasing rate from the present five or six percent to some 10 or even 15 per cent over the next year or two’ A year later prices increases were running close to 10 per cent and within two years inflation was higher than 15 per cent. Mr Peter Jay the Economics Editor of The Times wrote The boom that must go bust in May 1973 providing what Lord Harris described as' a classic diagnosis of the acute stages of an inflation reverb that it was still being fed by massive government expenditure, budget deficits and monetary and incontinence’. Other prominent dissenting monetarist perspectives in the early 1970s included those of Sir Samuel Brittan’s columns in The Financial Times and Mr Gordon Pepper’s writing in Greenwell Montague’s Monetary Bulletin.

By 1974 it was clear that the post-war Keynesian paradigm was finished

The problem with British economic policy at the start of the 1970s was that the post war Keynesian macro-economic paradigm had broken down. Over the closure of each economic cycle inflation and unemployment were rising. There was not a stable relationship where some unemployment could be traded for less inflation. At the heart of this was the structure of labour market institutions that resulted from legislation such as employment protection and trade union power. High and unexpected inflation aggravated the problems of labour market institutions blunting the information that wage negotiators needed for realistic wages setting. The resort to micro-economic controls on wages and prices was having less effect when it did work, was creating more anomalies and distortions of incentives and were encountering greater opposition from trade unions that had become progressively more militant. In the Spring of 1974 the unions were further empowered and radicalised: having destroyed the effective operation of the Industrial Relations Act 1971, the Conservative Government's public sector pay norms, seen the NUM’s flying pickets break the statutory pay policy and forcing the Prime Minister to hold an election that he lost.

In terms of the broad criteria for assessing the success of macro-economic management set out by Harold Macmillan to his Cabinet in May 1962, Edward Heath’s government was a comprehensive failure. National Institute Economic Review published two days before the 28 February 1974 General Election, for example wrote ‘It is not often that a government finds itself confronted with a possibility of simultaneous failure to achieve all four main policy objectives - of adequate economic growth, full employment, a satisfactory balance of payments and reasonably stable prices’.

answer to the question” Did Rachel Reeve in July 2024 have the greatest economic problems of any chancellor taking office since Hugh Dalton in 1945?” is “no”. The structural economic problems facing the new Conservative Government in 1970 were much greater. They included entrenched structural problems in product and labour markets, a radical, militant trade union movement empowered by its success in destroying the previous Labour Government’s attempt to reform trade union law; an immediate acute inflation problem; and increasing evidence that the post-war Keynesian approach to demand management was no longer reliable, exhibiting an unstable Phillips Curve where there was no easy trade off between a given rate of inflation and certain level of unemployment; and both rising inflation and rising unemployment becoming the experience of each economic cycle.And if that was not enough, there had been the quadrupling of energy costs.

The economic crises between 1970 and 1974 offer several lessons that are useful

The policy response to inflation in the early 1970s, and the new opportunities presented by an adjustable or floating exchange rate, along with the Heath Government’s legislation on industrial relations law and the government’s management of challenging national strike action, yielded experience that is worth understanding. Among the lesson of this experience are:

micro -economic controls cannot successfully repress a sustained increase in the price level;

prices and Incomes policies may work for a short period of time but come at a significant cost in terms of damage to incentives, the creation of anomalies and the efficient functioning of an economy’s labour and product markets;

a flexible exchange rate makes managing pressures on the balance of payments much easier, yet it does not enable a country to abandon competent and prudent macro-economic policy in relation to fiscal and monetary policy;

a floating exchange rate in the context of accommodating monetary and fiscal policies that make a country’s exports uncompetitive through domestic overheating and inflation will expedite the pass through of higher import costs;

a flexible or adjustable exchange rate is not a substitute for effective domestic monetary policy;

structural changes in the the regulation of banking and credit markets such as Competition, Credit and Control can transform the supply of credit to the banking system in ways that are unexpected and difficult to manage;

there is a complex set of questions about the balance in monetary policy between market freedom and prudential control, the role of reserve requirement to control the supply of money and the role of using interest rates as a tool for controlling the demand for money;

it is very difficult to disinflate and economy without a temporary increase in unemployment above the rate that would normally prevail in an economy reflecting its labour market institutions;

macro-economic policy cannot get unemployment below the rate yielded by labour market institutions such as the behaviour of trade union negotiators, the structure of industrial relations law, employment regulation and the effects of the tax and benefit system;

a full fiscal reflation backed by an accommodating domestic monetary policy and falling exchange rate cannot raise the trend rate of economic growth: it will simply result in inflation and a balance of payments problem;

government intervention, industrial strategies, nationalised industry investment plans will not effectively modernise economies or enable industrial economies to avoid the effects of de-industrialisation when firms and industries cease to be competitive in home and foreign markets reflecting a loss of comparative advantage;

public sector pay has to be controlled as part of the overall control of public expenditure and managing the public sector and nationalised industries efficiently is a challenge for governments;

the miners’ strikes of the 1970s demonstrated that governments in democratic states need an infrastructure of emergency planning, law enforcement and policing to enforce normal law, contract and court decisions when radical workers or politically organised groups decided to override the conventional operation of the law;

when a consensus on macro-economic management is shown to have become redundant it is not easy for policy makers to construct a workable alternative framework of policy.

The collapse of the Bretton Woods system of fixed priorities was an opportunity for economies, such as France, West Germany, Japan, Switzerland and the UK to have greater discretion in both managing their external accounts and avoiding importing US inflation, yet only Germany and Switzerland and arguably Japan took full advantage of these opportunities.

Moreover, when it came to absorbing the lessons of the monetary counter-reformation in macro economics led by American economists, such as Milton Friedman and Anna Schwartz, and translating their ideas into workable monetary policy, in the early 1970s, it was only Germany and Switzerland that managed to do so

Both the United Kingdom and the United States found it difficult to do so, in an orderly and sustained manner over the next ten years, creating a new macro-economic model with an appropriate framework for evaluating and applying monetary policy would be a continuing awkward challenge for future British governments.

The legacy of the Heath Government for Labour ministers in March 1974

In March 1974 Labour Ministers inherited an economy where trade union power was unbridled by law and exercised in a politically militant manner; an incomes policy with threshold clauses indexed to inflation, when high inflation was about to rise further that would turn them into pay escalator clauses; quadrupled oil prices; a balance of payments that was haemorrhaging; company profitability that had been destroyed by the combination of inflation and the way that price controls and pay policies operated; and a Keynesian economic paradigm that had effectively collapsed with few clearly developed ideas at the top of the Treasury, Bank of England or in much of the Government Economic Service of what to replace it with. These are much greater difficulties than those that Rachel Reeves has had to manage as Chancellor of the Exchequer since July 2024.

Warwick Lightfoot

26 September 2024

Warwick Lightfoot is an economist and was Special Adviser to the Chancellor of the Exchequer between 1989 and 1992.