Labour’s Budget: a backward looking rhetoric of nostalgia, that exaggerates tax increases for presentational purposes

The political economy of new British Labour Government’s budget, continuity and the zeitgeist of atavistic intergenerational focus on distribution that colours its construction

This article looks at the political economy of Labour’s first budget and its distinctive political context. That context is a growing focus on growth in the value of capital assets, the dispersion of capital ownership and distributional equity which informs most of the budget’s individual tax measures. The thinking informing the budget tax measures, draws on a debate among the community of left-wing think-tanks over the last twenty years. It is a debate that the Chancellor Rachel Reeves has herself contributed to. This interest in distribution has resulted in an unfortunate series of arguments that sets the stage for intergenerational conflict. It was not an accident that the first measure the Chancellor announced was the means testing of winter fuel payments for pensioners. It played to a gallery of supporters of intergenerational distributional conflict among a community of economists and researchers that shape contemporary thinking. In many respects the budget represents continuity with a form of ‘uniparty’ economic policy agenda, with a lot in common with policy developed by previous Conservative governments.

Political nostalgia for collectivism

Rachel Reeves, the Chancellor of the Exchequer in the Labour Government elected on 4 July 2024, presented the Government's first budget on 30 October . The Chancellor framed the budget in a rhetoric of nostalgia invoking the historic folk memory - 1945, 1964 and 1997. It looks backward. The Chancellor’s thinking is variously located in a combination of 1940s collectivism, a naive belief in technology and scientific innovation; and large discretionary increases in spending on public services, taxation and borrowing, ornamented with convoluted fiscal rules that accommodate increased spending paid for by borrowing.

A Pedestrian if not leaden parliamentary performance

Budget statements are political events. The Chancellor is a self described social democrat. She took no part in Labour’s front bench when Jeremy Corbyn led the Labour Party, which suggests an edge of robust principle.The manner in which budget speeches are delivered can establish a chancellor’s political authority. A light engaging personality at the dispatch box in the House of Commons can establish a chancellor’s political reputation. Both Harold Macmillan and Roy Jenkins benefitted from their budget speeches. Macmillan’s would still probably be scored as the funniest budget speech since the end of the war in 1945. Roy Jenkins' distinctive elegance and parliamentary elan contributed to his authority as a politician. As part of the theatricality of British parliamentary politics a budget speech offers a chancellor an unusual opportunity. Rachel Reeves was unable to take advantage of that opportunity. The Chancellor was pedestrian, when not leaden, in her parliamentary manner. She punctured her speech with clumsy contrived political jokes directed at her opponents. Worked up political jokes on the floor of the House of Commons are usually tedious. Rachel Reeves simply made her speech longer and more convoluted by attempting something she was unable to carry off.

A hodgepodge of measures whose overall scale has been exaggerated by the Chancellor

In the 1980s a shrewd political journalist, Ronald Butt described a Conservative Cabinet minister as appearing to want to say something, but suffering from not knowing what he wanted to say. Rachel Reeves' Budget speech conveys the same impression. It amounts to a huge hodgepodge of measures. They appear to have little economic coherence. The Chancellor chose to emphasise that the budget would raise taxes by £40 billion. This is obviously a big cash figure. Yet it has been ‘bigged up’ in its presentation by her. Over four years tax will cumulatively rise by over £40 billion in an economy of £3,400 billion. This raises the tax burden as a share of GDP by a little over 1 per cent during the period.

The political authority of the Chancellor has not been enhanced by the disjuncture between Rachel Reeves’s rhetoric in the General Election and the lurid, ‘it's going to be hard’, we will have to take ‘tough decisions’ rhetoric of the Prime Minister and Chancellor, since the election. They had both promised that apart from an extension of the VAT base to private education and the ending of the unusual tax status of wealthy foreign non-domiciled residents, there was going to be no discretionary increase in general taxation. The Prime Minister and Chancellor promised no tax change, after all taxes were said by Rachel Reeves to be too high.

Labout’s Budget is part of a continuity uniparty approach to framing government policy

Yet in office the Chancellor has sought to be perceived to be doing something big. She has used exaggerated rhetoric to describe the cumulative effect of the sort of decisions made by an administration applying a ‘uniparty’ government approach to the public finances and economic management. This allows the ratio of government spending to GDP to drift upwards over the economic cycle. The striking thing is the continuity between the substance of the policies of the new Labour Government and its recent Conservative predecessors, the fiscal rules, the use of fiscal drag to raise revenue, the raising of national insurance rates and the rhetoric about the role of investment in economic growth. This is reflected in the former Conservative Business Secretary, Greg Clark’s welcome of the Government’s industrial strategy in an interview in the THE - the Times Higher Educational supplement. Rishi Sunak, both as Chancellor and Prime Minister, had raised the tax burden to a historic high through the ending of indexation of income tax allowances and thresholds and the resurrection of full fiscal drag aggravated during episodes of inflation. Sir Keir Starmer and Rachel Reeves constructed a formula that working people would not pay more tax and there would be no increases to the principal revenue raising source of receipts income tax, VAT and national insurance.

Campaigning in poetry, governing in prose or saying one thing in Opposition and doing something else in Government?

The Chancellor has now increased employers’ national insurance and lowered its threshold for payment. The impressively articulate Chief Secretary to the Treasury, Darren Jones has been forced to dance on the head of a pin. Employing great linguistic imagination to argue that such a measure would not increase taxes on working people. When plainly the incidence of the tax increase, and it is a significant tax increase, scored at £25 billion, would do so. In political terms, the Chancellor has sold an insurance policy in the election, but drafted its small print in a way that has ensured there is plenty of scope not to pay out on a claim. Hence, the succession of measures raising inheritance and capital taxes, as well as an increase in the transactions tax on certain property purchases, to be used as second homes or let as private rental properties, that Britain quaintly calls ‘stamp duty’.

Losing control of expectations and setting off an intense debate about taxation of savings, capital and pensions and the treatment of pensioner benefits

By announcing the means testing of the heating allowances for pensioners in July and employing the gloomy rhetoric ahead of the Budget the Treasury and 10 Downing Street lost control of expectations and budget speculation. Ahead of budgets the Treasury sometimes does a bit of ‘there will be blood on the carpet ‘pre-budget speculation only to make some minor changes to tax that are greeted by happy relief. The extraordinary speculation that the Treasury allowed has undermined the trust that Sir Keir Starmer and his Chancellor carefully established in Opposition.

Increasing unpopular salient taxes on savings and capital

Worse from the Chancellor’s political perspective, much of it focused on unpopular taxes that are salient, such as inheritance tax, the taxation of savings and pensions. Among the things openly speculated about were the end of the tax free pension 25 per cent lump sum, applying capital gains tax, CGT, at full income tax marginal tax rates without indexation, full CGT on death, before the application of inheritance tax, and a severe cap on the cash value of investments that enjoy expenditure tax treatment, when held in an in ISA saving wrapper. Even more extraordinarily there was speculation that the spousal exemption in inheritance tax would go.

If the Winter Fuel Payment goes, what about the Bus Pass?

Having ended the winter fuel payment for pensioners there was inevitably speculation about the future of the Elderly England Bus Pass. The Government was not sufficiently adroit to dispose of a provocative teasing question put to Lord Hendy, the Labour Transport Minister in the House of Lords. Lord Moylan asked the minister if he could reassure the public that the bus pass would not be subject to means-testing as well. The following day after Lord Hendy’s carefully evasive answer in the Lords, a Treasury Minister in the House of Commons, when further asked about Lord Hendy’s circumspection on the matter, refused to rule out the ending of the bus pass. Throughout the summer and autumn months at bus stops in provincial England - a separate free bus, underground and rail pass operates in Greater London - bus passengers openly speculated about how long the Elderly England Pass would continue.

An agenda of distributional equity and a connected atavistic intergenerational conflict

There is a connected community of researchers and left wing think-tanks that amplified pe-budget speculation about tax increases.There are many engaging, clever, well trained economists working in left of centre think tanks that speculate about distribution of income and wealth and occupy themselves suggesting changes in taxation of savings, pensions and capital. The IPPR, the New Economics Foundation, the Wealth Commission and the Resolution Foundation are examples of these organisations. While their interests focus on distribution and a lowering of the Gini coefficient, they pay less attention to taxation as a source of revenue receipts that yield money to pay for public services and the kind of services, transfer payments and functioning markets that help people living persistently in the bottom fifth of the income distribution. Rachel Reeves has contributed to this literature as an MP suggesting among other things that the amount of capital invested in an ISA should be limited.

This network of left of centre think-tanks, as well as stimulating a discussion about the distribution of capital, and the taxation of wealth, has contributed to a debate that sets one generation against another. This has been initiated by a former Conservative Minister Lord Willetts the chair of the Resolution Foundation in an interesting book The Pinch. The main burden of his book is that the baby boomer generation have benefitted from things that the generations that followed have not enjoyed. These include higher education without tuition fees, a housing market with lower costs in ratio to income, and better access to generous final salary occupational pensions. It always glossed the ending of full employment in the mid-1970s, massive youth unemployment in the late 1970s and 1980s, the fact that few people ever got to enjoy full, final salary defined benefit schemes - because early leavers were penalised - or the changes in transfer payments to households of working age that developed in the 1980s and after 1997, the reform of the State Earnings Related Pension SERPs that reduced its benefits in 1987, and the decision to uprate the basic state pension by inflation and not earnings between 1981 and 2010. This has set generation against generation. It has resulted in a generation of younger researchers losing sight of the role the tax and benefits system performs in smoothing incomes over the life cycle that inevitably involves paying benefits to retired pensioner households.

Part of this research agenda has responded to an atavistic intergenerational squabble that concentrates on the distribution of savings and wealth. Inevitably the households that normally have accumulated most savings, financial assets and property wealth are older households. The saving has been carried out for use when they cannot work. Lord Beveridge in the 1940s was explicit about this. The basic national state pension, as the basis of pensioner living standards and people were expected to save and accumulate assets to supplement it. This is what UK households have done. The result is that they are in possession of more capital and savings than younger households. That is part of the life-cycle of saving. My late grandmother's irritatingly expressed aphorism was: ‘economy is the armchair of comfort in old age’.

The focus on distribution and inequality has resulted in attention concentrating on the dispersion of savings and wealth. A good example of it was the Resolution Foundation’s excellent conference on wealth, taxation and the opportunities for introducing a wealth tax in September 2024. The inspiration for the conference was the tenth anniversary of the publication of Thomas Picketty's book Capital in the Twenty-First Century, the increases in housing and financial wealth since 2009, and greater dispersion of the ownership of capital in the USA. The increase in the value of financial assets and property reflected the monetary response to the Great Recession and the use by central banks of Quantitative Easing to increase financial wealth as an economic stimulus. Household wealth has increased from three times GDP to seven times GDP in 2019. The Gini coefficient that measures inequality in th eUK, however, is little changed. The flow of income generated by those assets has not risen and the dispersion of income in the UK has narrowed.

Most of the tax changes that attract the interest these researchers involve aggravating the double taxation of saving, inherent in an income tax system. Their fancies often involve great complexity, the requirement of taxpayers keeping extensive and inconvenient records and in highly salient taxes that raise little revenue.

A public sector sensibility that overlooks the difficulties of complex tax collection and flows of income

Much of this thinking reflects specific cultural sensibilities. Many of the people involved in this thinking come from comfortable families whose parents worked in the public sector. The distinguishing feature of public sector employment - teachers, health workers, nurses, doctors, people working in higher education, local authority officers and civil servants - is reliable, largely index linked for inflation, final salary, pension schemes. Public sector pensions enable their beneficiaries to move around from employer to employer and location to location. Moreover, employees in the public sector tend to enjoy greater stability in employment than people working in the private sector. The result is that they accumulate substantial occupational pensions, compared to most people working in the private sector. As a result they do not have to rely on private final contribution schemes or the accumulation of assets in ISAs. They tend to have little practical experience of running businesses, managing vulnerable balance sheets and facing the anxieties of awkward cash flow. This results in naivety about high marginal tax rates. They have lives that are immune from having cash available to pay tax bills in January and July that are often lumpy in relation to the flow of incomes over several years, the awkwardness of reliable record keeping and the expense of employing professional assistance with payrolls, accountancy, investment and savings advice. In many respects the Chancellor exemplifies this public sector sensibility - the daughter of two teachers, who became a Bank of England official and married a civil servant. Mark Carney the former Bank of England Governor has spoken of the difference between the seminar room and practical policy. A compelling case for taxing all capital gains on an accruals basis at a Nuffield College Seminar, on a wet afternoon in Oxford, can fall apart in contact with the outside world.

Practicality in tax collection - can they pay the bill, have they got the cash?

It is, moreover, a zeitgeist that is not informed by practicality. Taxes have to be affordable in the sense that the burden should fall on a taxpayer who has the money available to pay it. There are therefore limits on the amount of tax that can be collected from property in relation to its value. Taxes can be levied on flows of income and spending and when events take place such as the sale of an asset. Levying taxes on a change in capital values on an accruals basis is not practical when the taxpayer does not have the cash to pay the bill without liquidating the asset. This is why CGT is levied when an event crystallises a tax liability, such as a sale or a transfer of ownership. That is why taxes are levied on death and only on the death of the final remaining spouse. That is why the taxation of the imputed rent of an owner occupied house under schedule A - the income tax of land - was abolished by the Macmillan Government. As owner occupation increased and income tax through fiscal drag descended down the earnings distribution, more and more people were drawn into paying it on their own homes. Many found it difficult and it was a highly salient and unpopular tax. That is why Selwyn Lloyd abolished it in the early 1960s.

Labour Pre-Budget Speculation: hyperbole and anxiety

These instincts have not been confined to think-thanks advising the Labour Party. The Conservative governments between 2015 and 2024 were capable of similar thinking in relation to industrial strategy, artificial investments to stimulate investment, changes to the private rented sector and measures directed at pushing out small private landlords from the rented housing sector . The Chancellor’s statement in July when she described a £22 billion black hole in the public finances requiring painful tax remedies, however, set-off an extraordinary flurry of anxious speculation that went beyond normal pre-budget guessing games.

Budget measures directed at pensioners, savings and capital

It was not an accident that the first measure announced was the scrapping of the winter fuel allowances and restricting its payment to means tested pensioners on pension credit.The allowance had been introduced by Gordon Brown at time when energy prices were lower, it supplemented a basic state pension that is low as a replacement ratio of earnings. The UK has one of the lowest basic state pensions among advanced economies. Moreover, once occupational pensions are taken into account UK pensions remain low when benchmarked internationally.The Chancellor’s first decision to lower the basic non means tested state pension income, by restricting winter fuel payments was a direct response to this awkward myopic focus on distribution and intergenerational differences in savings. It involves a high political price for little fiscal gain.

Pre-Budget speculation damaged consumer, business and investor confidence and provoked at behavioural response among savers and investors: liquidation

Pre-budget speculation set off a behavioural response from economic agents. This was reflected in falling business, investment and consumer confidence ahead of the budget. Wealthy households began to move abroad. People decided to take their tax free lump sums from pension funds, on such a scale that financial advisers and pension fund trustees could not keep up with the administrative work involved. Investors in AIM shares held because of their exemption from inheritance tax began to sell them creating disorderly markets in what are often relatively illiquid markets in terms of price discovery. Assets were sold ahead of fears of CGT being levied against marginal tax rates without indexation. People holding assets in ISAs sold them to crystallise long term gains in case they were dismantled by the Chancellor. A good example of this was Lord Lee, the ubiquitous ISA millionaire investor's decision to liquidate many of his longstanding and highly profitable holdings.

Will one Tax raid be enough for Labour’s Chancellor ?

In the end the scale of the budget in terms of tax increases was relatively modest.There was huge relief for many many people after the speculation ahead of the budget. The big increaseases in public spending for investment being financed with borrowing. The difficult question to gauge is whether economic agents will take the Chancellor at her word when she says that the tax raising package was a one-off reset that would not be repeated. The response of the gilt market is not encouraging. Investors Chronicle editorial could not be blunter : Will this £40 billion raid be enough? This suggests that the jury is very much out.

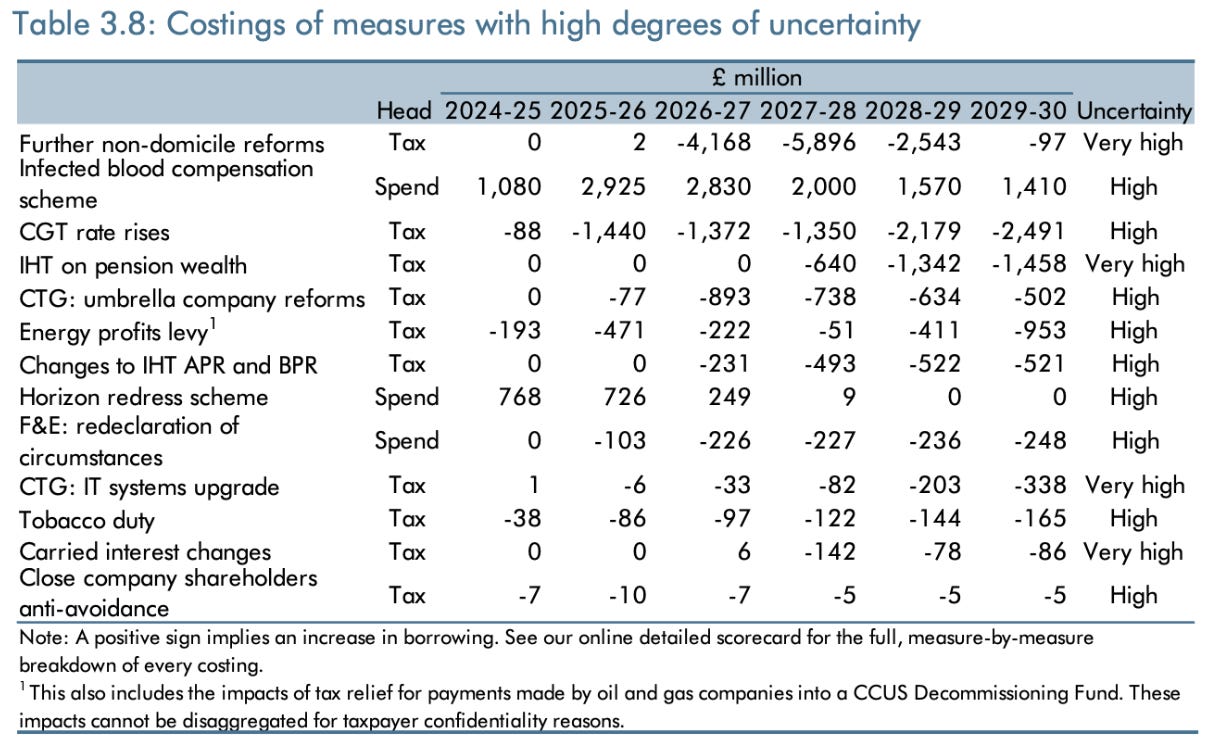

Not least, because the Chancellor chose to touch so many reliefs - farmers, business assets, owners of defined contribution pension funds and private landlords - all had tax measures applied to them. Yet the revenue yielded by the measures is modest and will be uncertain, as the OBR has pointed out in Table 3.8 Costings of measures with high degrees of uncertainty in its Economic and fiscal outlook. It is not clear how realistic the revenue forecasts are. As Ian Stewart the chief economist of Deloitte noted in his Deloitte Monday Briefing that ‘the margin of error for the government to meet its fiscal target is slender. In an economy where GDP runs at £2.9 trillion annually and public expenditure is £1.3tn, leeway of £10bn to meet the government’s debt rules allows little room for things to go wrong. £10 billion of fiscal headroom is the second lowest in the last 14 years and about one-third of the average’.

This article has concentrated on the political economy of the Budget, the growing debate about capital taxation and the tax measures directed at taxing capital. Further pieces will explore the budget’s economic forecast, the effect of policy measures on the labour market, and the large discretionary increase in public spending.

Warwick Lightfoot

4 November 2024

Warwick Lightfoot is an economist and was Special Adviser to the Chancellor of the Exchequer from 1989 to 1992.